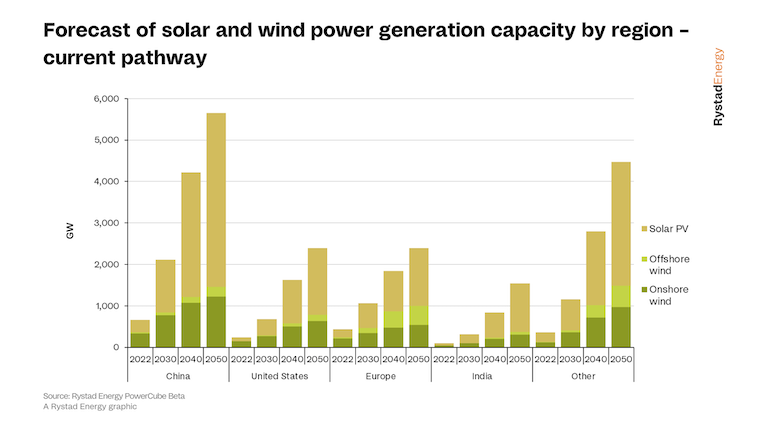

Mainland China is the largest consumer of electricity in the world and the largest emitter of carbon dioxide (CO2). It is also developing more renewable energy capacity than any other country and has a target of reaching carbon neutrality by 2060. During the recent COP 27 negotiations in Egypt, China pledged to reach peak emissions by 2030 and is still willing to discuss the global goal of limiting global warming to 1.5 degrees Celsius (°C) above pre-industrial levels. The country’s power sector, which contributes more than 40% to China’s greenhouse emissions, will play a critical role in achieving those ambitions – both by decarbonizing itself and other sectors. Rystad Energy forecasts that China’s renewable energy growth will continue on a steep upward trajectory that could see it reach close to 6,000 gigawatts (GW) of installed solar PV and wind capacity by 2050.

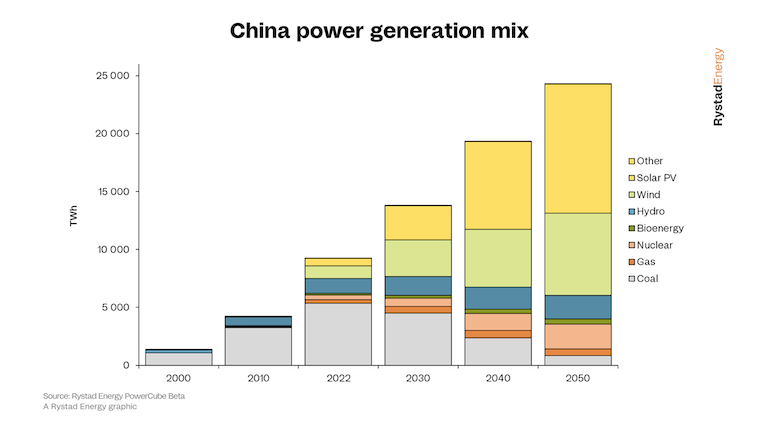

China’s electricity consumption this year is expected to total 7,400 terawatt-hours (TWh). Around 58% of this power is generated from coal-fired power plants, followed by hydro with 14% and wind with 12%. In the last 20 years, China prioritized the development of coal-fired generation capacity, which will total 1,115 GW this year. Using its large coal reserves to provide an affordable source of energy, this has powered the country’s economic growth and limited its dependence on energy imports. Since 2010, however, China has also been diversifying its power mix, installing 160 GW of hydro capacity, 46 GW of nuclear, 360 GW of solar PV and 360 GW of wind, making it the largest developer of renewable energy capacity worldwide.

China’s electricity demand is expected to continue growing at a fast pace, meaning that substantially more new renewable energy capacity will be needed to meet growing demand and to replace existing fossil-fueled generation. Power demand is forecast to reach 13,600 TWh by 2050, with most of the growth coming from the transport sector. Other sectors, such as industrial and residential, are also expected to grow at a faster pace as fossil fuels are gradually replaced by electricity as a primary source of energy. In total, over 6,200 TWh of new electricity supply will be needed to meet future demand.

China currently has at least 25 GW of coal generation capacity still under development, which is due to push coal-fired capacity to a peak of 1,140 GW by 2025. However, coal generation could peak as early as 2023 as output from old coal-fired power plants is replaced by fast-growing renewable energy. Installed gas-fired generation capacity, by contrast, is forecast to continue growing from 112 GW in 2022 to 355 GW by 2050, helping replace coal plants and providing base load – and flexibility – to the system. Given that gas generation emits around half as much CO2 as coal generation, growth in installed gas generation capacity is not expected to increase China’s total emissions and, as such, it is likely that its global warming emissions from the power sector could peak in 2023. With the power sector being the largest source of emissions, this would put China’s power sector on track to help meet its target of peaking emissions by 2030, although emissions from other sectors would still need to be addressed.

“China is ahead of the game; coal use in the power sector is set to peak in two years’ time and new renewable power is coming online faster than any other country. Economics favoring renewables and domestic solar manufacturing capacity means that China’s power sector could rapidly decarbonize by 2050. China has all the pieces needed to scale renewables rapidly and the extent of its success will have a global impact on global greenhouse gas emissions, ” Says Carlos Torrez Diaz, head of power at Rystad Energy

Current renewable energy targets would put country on 1.9°C pathway

During COP 26, held in the UK in late 2021, China announced its target of lifting total installed solar PV and wind capacity to 1,200 GW by 2030 compared to 745 GW in 2022. Current developments suggest China will not only meet this target but could surpass it and increase total installed capacity to around 2,000 GW. This would cement the country’s leadership in renewable energy capacity.

The 6,000 GW of renewable capacity set to be installed by 2050, plus the 540 GW of hydro and 296 GW of nuclear power, would be enough to generate 91% of the country’s electricity from fossil fuel-free sources this year. Given that the levelized cost of energy (LCOE) for solar PV and onshore wind is, under optimal conditions, now below that of coal and gas power, it makes sense for China to develop as much renewable capacity as is technically possible. The LCOE of solar PV in China is currently estimated at around $50 per megawatt-hour (MWh) compared to more than $80 per MWh for a new coal plant and $55 per MWh for existing plants. This development is especially feasible in China, which has more than 90% of existing global solar panel manufacturing capacity, meaning panels can be supplied at affordable prices.

Despite positive outlook for renewables, more is needed to reach 1.5°C

Current project developments, manufacturing capacity and policies are guiding China in the right direction of lower emissions. In order for it to help limit global warming to 1.5°C, however, an even faster decline in fossil-fueled power generation will be needed in China. In Rystad Energy’s current pathway scenario, we see that there would be around 1,000 megatonnes of emissions from the power sector remaining by 2050. Even if some of these emissions could be stored using carbon capture and storage (CCS) technologies, more will need to be done to help emissions drop closer to zero megatonnes by 2050 to help limit global warming.

Current project developments, manufacturing capacity and policies are guiding China in the right direction of lower emissions. In order for it to help limit global warming to 1.5°C, however, an even faster decline in fossil-fueled power generation will be needed in China. In Rystad Energy’s current pathway scenario, we see that there would be around 1,000 megatonnes of emissions from the power sector remaining by 2050. Even if some of these emissions could be stored using carbon capture and storage (CCS) technologies, more will need to be done to help emissions drop closer to zero megatonnes by 2050 to help limit global warming.

Rystad Energy forecasts that global emissions will need to peak this year and drop below 9,600 megatonnes by 2050 for the world to remain on track to limit global warming to 1.5°C. Given that China is and will continue to be the largest emitter of CO2, the country’s actions play a central role in this. During COP 27, China’s environmental envoy did not oppose mentioning 1.5°C as a goal for limiting global warming, giving some hope that developments could move faster in the right direction.

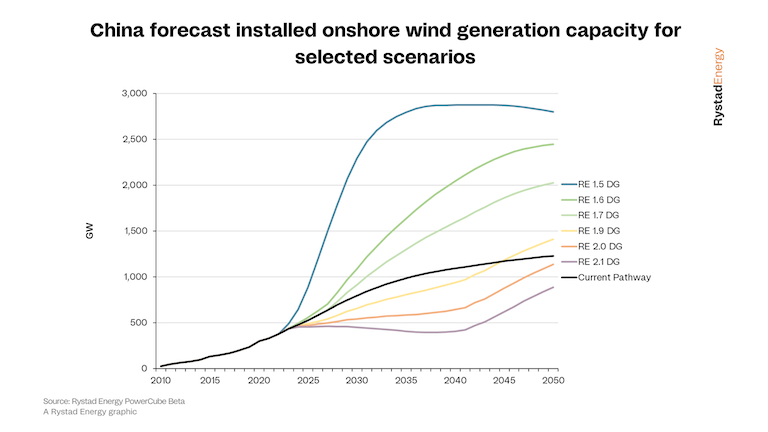

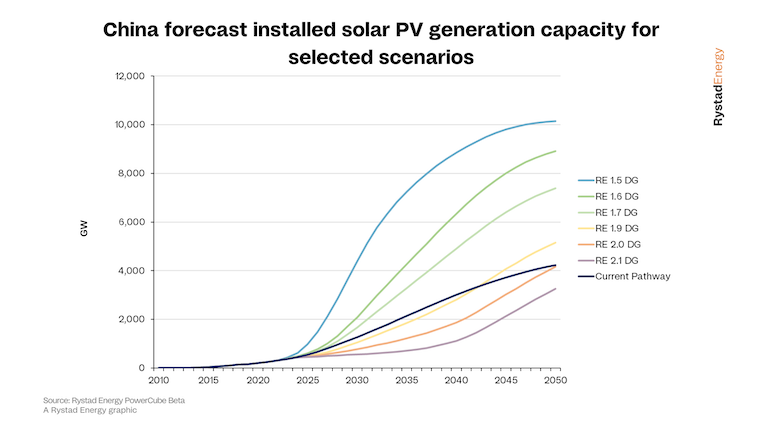

In the current pathway scenario described above, China’s power capacity developments would be enough to help limit global warming to 1.9°C. To keep on track to meet Rystad Energy’s 1.5°C scenario, more than twice as much solar PV and onshore wind capacity would be needed in China by 2050. This would enable China to displace coal generation at a much faster pace, reducing emissions from the power sector to close to zero megatonnes by 2050. Besides the faster deployment of renewable energy capacity, China would need substantially more battery storage capacity to help back up the intermittency of renewables. In the 1.5°C scenario, a forecast 4,300 GW of battery storage capacity would be needed by 2050 compared to 1,084 GW in the current pathway scenario.

The 1.5°C goal is very ambitious but could still be feasible. China is the world’s largest manufacturer of solar PV panels with current manufacturing capacity of 425 GWAC per year, which is expected to reach 613 GWAC per year by 2030. The existing capacity is already enough to achieve the country's needed average annual installation rate of 350 GWAC of solar PV to stay within 1.5°C global warming but this would imply reducing panel exports. To help meet domestic demand and remain as the largest exporter of renewable energy technology, investments will have to continue flowing into China’s renewable energy space. This appears achievable given that the country has already bet on renewable energy and battery technologies to help power its economy in a sustainable manner.

Follow us on social media: