Air cargo tonnages from Asia Pacific to Europe and North America have bounced back strongly in the last two weeks from their Lunar New Year holiday lull, with some signs of the worldwide market stabilizing following months of demand and rate declines.

After having reported last week that worldwide air cargo tonnages recovered faster and more strongly this year in the initial weeks since the annual Lunar New Year holiday downturn, we see now a continuing stabilizing trend for both tonnages and the global average rate, albeit significantly lower than those of early 2022, the latest preliminary figures from WorldACD Market Data indicate.

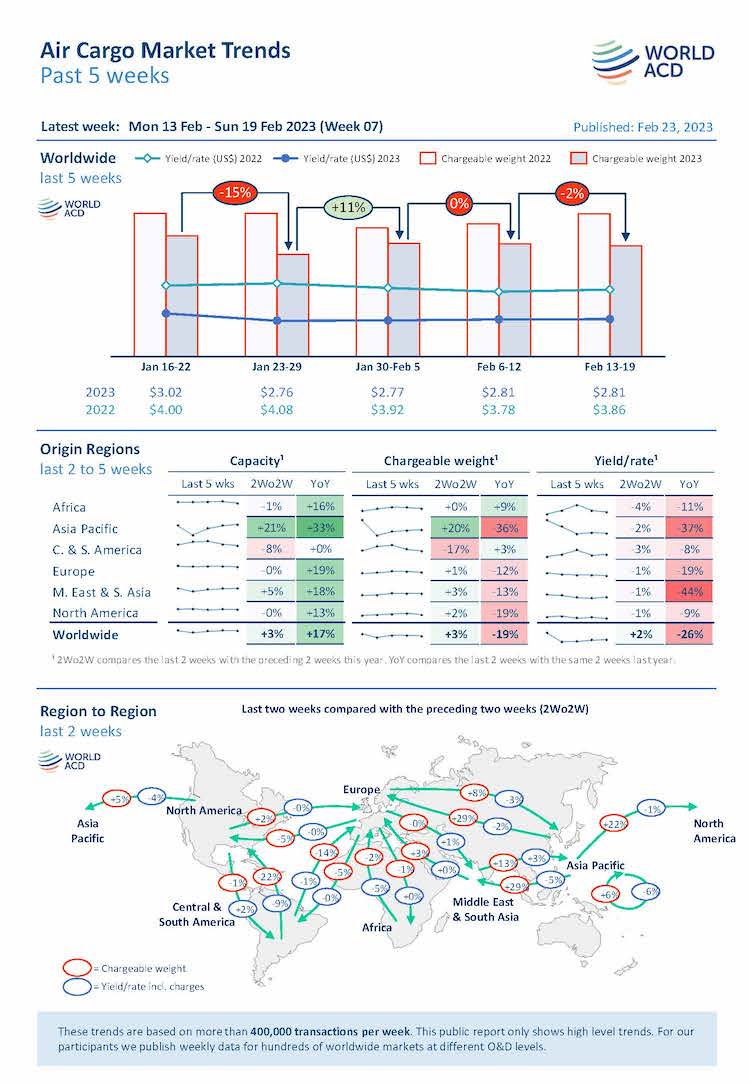

Figures for week 7 (13 to 19 February) show a small decrease (-2%) in worldwide tonnages compared with the previous week. On the pricing side, global average rates remained completely stable compared with the previous week, although underlying regional trends can differ strongly, particularly related to Asia Pacific.

Comparing weeks 6 and 7 with the preceding two weeks (2Wo2W), tonnages are up +3% above their combined total in weeks 4 and 5, accompanied by a +3% increase in capacity, whereas average worldwide rates went up by +2% – based on the more than 400,000 weekly transactions covered by WorldACD’s data.

At a regional level, on a 2Wo2W basis, the post-Lunar New Year recovery in air cargo tonnages was still very notable on ex-Asia Pacific flows to Europe (+29%), Middle East & South Asia (+29%) and North America (+22%), respectively. The most-notable decreases were recorded from Central & South America to North America (-22%) and to Europe (-14%), for a large part driven by the pre-Valentine’s Day flower export surge.

Despite volumes rebounding in recent weeks, on the pricing side the average rate for flows originating in Asia Pacific have continued to show a negative trend, particularly on intra-Asia Pacific (-6%) and to Middle East & South Asia (-5%).

Year-on-Year perspective

Comparing the overall global market with this time last year, chargeable weight in weeks 6 and 7 was down -19% compared with the equivalent period last year. Most notably, tonnages ex-Asia Pacific are down by -36%, although this comparison is skewed because Lunar New Year started ten days later last year, on 1 February compared with 22 January this year. There were also double-digit percent year-on-year drops in tonnages outbound from North America (-19%), Middle East & South Asia (-13%) and Europe (-12%). Tonnages outbound Africa were on the rise compared with the previous year (+9%).

Overall capacity has jumped by +17% compared with the previous year, with positive developments from all regions including Asia Pacific related to post-Lunar New Year recovery. The most-notable increases were ex-Europe (+19%), ex-Middle East and South Asia (+18%) and ex-Africa (+16%).

Worldwide rates are currently -26% below their levels this time last year, at an average of US$2.81 per kilo in week 7, despite the effects of higher fuel surcharges, but they remain significantly above pre-Covid levels.

Follow us on social media: