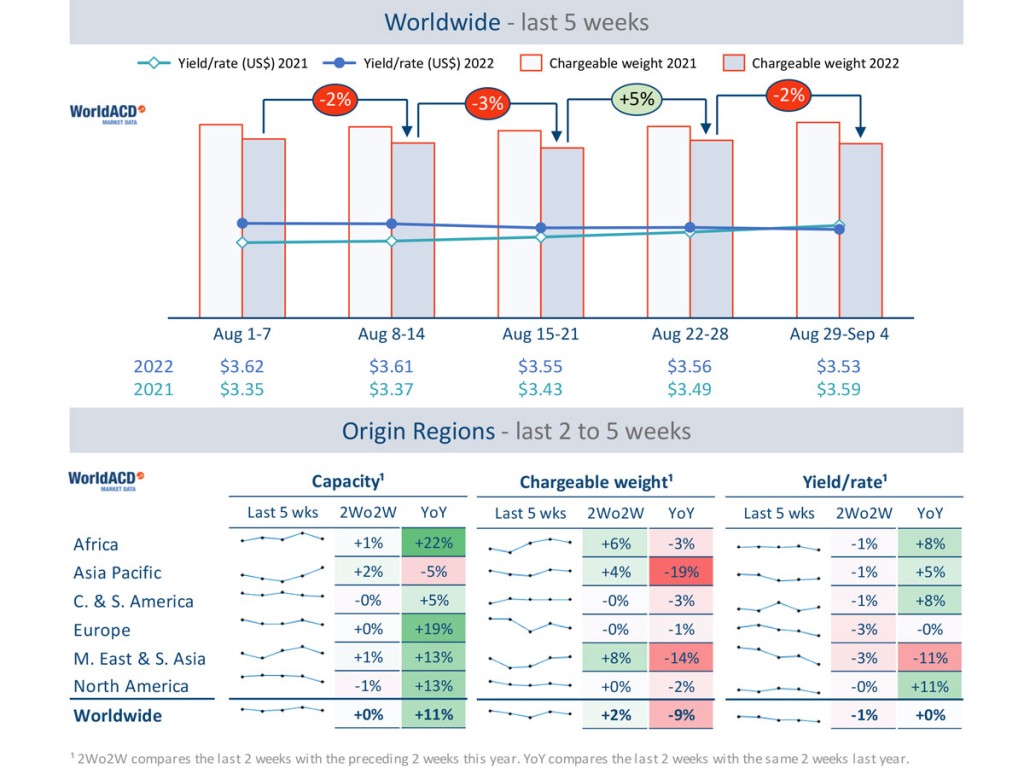

Worldwide air cargo tonnages dropped again slightly in the final few days of August and into early September after rebounding in the last full week of last month, the latest figures from WorldACD Market Data reveal. However, on a two-week basis they stand slightly above their levels in mid-August - suggesting a possible stabilization of demand, albeit below last year’s elevated levels.

Looking at week 35 (August 29 - September 4) alone, worldwide chargeable weight decreased -2% compared with the previous week, partly eroding the +5% week-on-week rise in volumes reported in week 34, while the average worldwide rate slightly decreased, based on the more than 350,000 weekly transactions covered by WorldACD’s data.

But comparing weeks 34 and 35 with the preceding two weeks (2Wo2W), volumes in the last two weeks combined are slightly up (+2%) on a 2Wo2W basis, while average worldwide rates declined -1%, in a more or less stable capacity environment.

Across that two-week period, tonnages showed signs of recovery from most of the main air cargo origin regions. Notably, volumes were up +4% from the key Asia Pacific origin region, on a 2Wo2W basis, and increased significantly from Middle East & South Asia (+8%) and Africa (+6%).

Those volume trends can also be reported on a lane-by-lane basis, with significant increases from Middle East & South Asia to Europe (+11%) and Asia Pacific (+19%), and from Africa to Europe (+6%), while the major lane from Asia Pacific to Europe saw a +4% increase. Intra-Asia Pacific volumes were also up +6%, and the strong US dollar relative to European currencies may have helped support a +3% rise in tonnages from Europe to North America.

Declines in volumes were in particular recorded on flows between Europe and Central & South America (outbound -5%, inbound -6%) and from Europe to Africa (-6%), on a 2Wo2W basis.

Year-on-Year perspective

Comparing the overall global market with last year, chargeable weight in weeks 34 and 35 was down -9% compared with the equivalent period last year, despite a capacity increase of +11%. Capacity from all of the main origin regions, with the exception of Asia Pacific (-5%), is now significantly above its levels this time last year, including double-digit percentage rises from Africa (+22%), Europe (+19%), North America (+13%) and Middle East & South Asia (+13%).

Meanwhile, after remaining above last year’s levels for the whole of 2022, worldwide rates have now slipped below (-2%) their level this time last year to an average of US$3.53 per kilo, despite the buoying effects of higher fuel surcharges compared with last year.

Follow us on social media: