South American spot LNG rises as Asia drifts lower

Jun 19, 2017

Spot LNG prices in east Asia have drifted lower over the past month, but renewed buying interest from South American countries to cover winter demand in the southern hemisphere pulled up LNG prices for the southwest Atlantic.

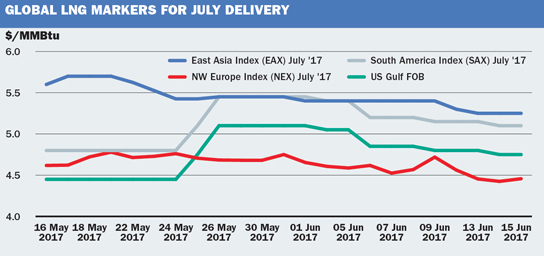

The ICIS July East Asia Index (EAX) for spot LNG averaged $5.450/MMBtu during its period as the front-month assessment, from 16 May to 15 June. This was down 4% from the previous month, as prices slid lower, with major buyers such as Japan and China largely keeping out of the market during the period. The EAX average was up 10% from the previous year.

Global LNG Markets for July delivery

Japanese utility sources said that volumes expected under long-term contracts would be sufficient to cover demand without requiring purchases from the spot market. The country’s Kansai Electric in early June restarted its 870 MW Takahama 3 and 4 nuclear reactors, bringing the number of operating reactors in Japan to five, compared with none at the same time last year. Increased nuclear power capacity reduces the need to buy LNG for gas-fired power generation.

Chinese buyers were seen to have some interest in spot cargoes, but were adopting a “wait-and-see” approach on prices, without an urgent need for additional supplies. Guanghui Energy’s new 0.6 mtpa Qidong regasification terminal received its first commissioning cargo in early June.

South Korean generator KOMIPO was looking for one spot cargo for July, and traders were waiting to see if there would be further demand from South Korea as a result of the Korean President’s decision to temporarily halt eight old coal-fired power plants in June to tackle a growing air pollution problem.

On the production side in the Asia-Pacific region, Australia’s 5.2 mtpa Gorgon LNG train 1 had a maintenance outage from 12 May to the end of the month due to problems with a flow measurement device. However, overall volumes across the three trains of the 15.6 mtpa facility did not suffer on a month-on-month comparison, with Gorgon loading 15 cargoes over the 16 May to 15 June period, up from 12 the month before. Gorgon has only recently opened its third production train.

Australia’s GLNG is expected to shut one of its two 3.9 mtpa trains in July for planned maintenance, but the market will soon see a boost from Chevron’s 4.45 mtpa Wheatstone train 1 expected to start up commercial deliveries in August.

Argentina buy tender lifts SAX prices

Argentinian gas company ENARSA entered the market in late May with a major tender for 16 cargoes to be delivered during July-October, ten for the country’s Escobar terminal and six for Bahia Blanca. The purchasing activity supported valuations for South American LNG, with suppliers including BP, Gas Natural Fenosa, Petrobras, Glencore and Trafigura heard to secure sales in the tender at prices around $5.00-5.50/MMBtu. Market sources also reported some buying interest from Brazil’s Petrobras.

The ICIS South America Index (SAX) averaged at $5.130/MMBtu during its time as the front-month assessment, only $0.320/MMBtu below the EAX.

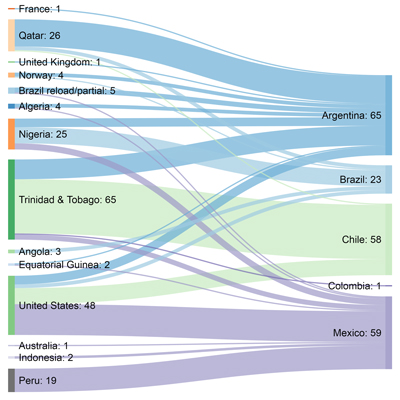

Key suppliers for South American countries include Trinidad & Tobago, the US and Qatar, which delivered some 65, 48 and 26 cargoes respectively to Argentina, Brazil, Chile, Colombia and Mexico combined over the year from June 2016 to May 2017, according to data from market intelligence platform LNG Edge.

Cargoes delivered to South America during June 2016-May 2017, Source: LNG Edge

For the longer-term there were also significant tenders launched by India’s Torrent Power, asking for 36 cargoes during the years 2018-2020 and from Turkey’s state-gas importer BOTAS, seeking some 19 cargoes to cover Turkey’s winter.

The NW Europe Index (NEX) held fairly steady over the course of the month, averaging at $4.636/MMBtu for July. This was below the EAX and the SAX, making Europe a less attractive destination for spot cargoes for most suppliers. Within Europe the UK remained at a discount to Continental Europe of around 20-30 cents per MMBtu for July and August, with the closure of the country’s main seasonal gas storage facility this year having reduced its summer demand.

US exports continue to build

Exports from the US continue to increase. The country’s Sabine Pass facility in Louisiana loaded 19 cargoes during 16 May to 15 June, up from 15 cargoes during the previous month. South Korea’s KOGAS, which has a long-term offtake agreement for train 3, loaded its first cargo on 3 June, onto the 174,000cbm, newbuild SM Eagle, and commissioning work is underway on train 4.

Sabine Pass sent its first cargoes to northern Europe in early June, with Norway’s Statoil taking a spot cargo to the Gate LNG terminal in the Netherlands and Sabine-operator Cheniere delivering a spot cargo to Swinoujscie in Poland. Statoil might normally have delivered a Norwegian cargo to Gate, but its Arctic Hammerfest LNG plant was out of action for planned maintenance until mid-June. Cheniere’s delivery to Poland is a symbol of Polish incumbent PGNiG’s desire to diversify its gas supplies, as well as of US aims to “reassure the energy security of … allies and partners around the world,” in the words of US Secretary of Energy Rick Perry.

Southern European countries including Spain, Portugal and Italy have been receiving US LNG since 2016. The UK is more likely to receive a Sabine Pass cargo in its winter, when NBP gas prices are expected to be higher than the Continent to pull Dutch and Belgian gas into the UK through interconnector pipelines to compensate for the ongoing Rough storage outage. The closure of the UK’s main seasonal gas store should act to reduce its summer gas prices but boost its winter prices.

Qatar continues to ship LNG

Exports of LNG from Qatar were largely unaffected in early June by the decision of neighbouring countries including Saudia Arabia, Bahrain, the UAE and Egypt to break off diplomatic relations. Qatari tankers continued to transit through the Suez Canal on their way to and from European customers, the neutrality of the canal protected by historic convention. Cargoes sourced from Qatar’s Ras Laffan production facilities continued to be delivered to Egypt’s Ain Sukhna regasification port. These cargoes typically arrive on ships chartered by Swiss-trading house intermediaries such as Glencore, Trafigura and Vitol. Qatar Petroleum said it was carrying on “business as usual.”

Shell was seen to divert one ship, the 173,000cbm Maran Gas Amphipolis, from Kuwait to the UAE in order to meet its supply commitments in the UAE without sourcing a cargo from Qatar. There was also market interest when two of Qatar’s largest tankers, the 266,000cbm Q-Max class Zarga and Al Mafyar, abandoned voyages through the Suez Canal to Europe to instead head southwards around Africa, but it was soon confirmed that these ships remained on course to ultimately deliver to the UK despite embarking on a longer route to get there.

by [email protected]

Whats this about?

It is the “uncontained” shipments that draw a lifetime allegiance of purveyors of the business. As one MPV (Multi Purpose Vessel) analyst bluntly said as an aside, “Boxes are boring.”

Follow us on social media: