"April brought fleeting peaks as tensions flared between Iran and Israel, nudging Asian spot prices to $10.44 per MMBtu.

Yet, with the threat receding, so too did prices, settling at $9.2 per MMBtu.

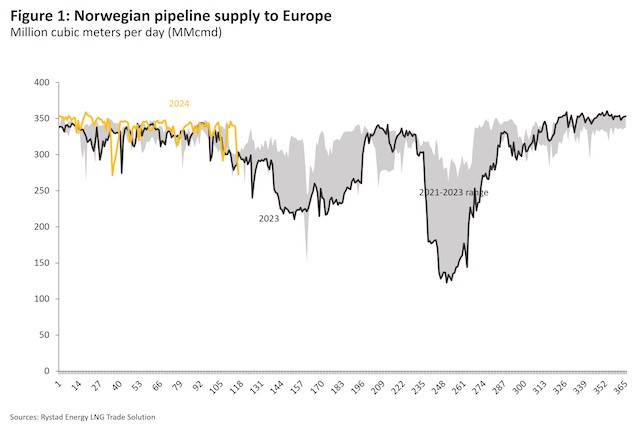

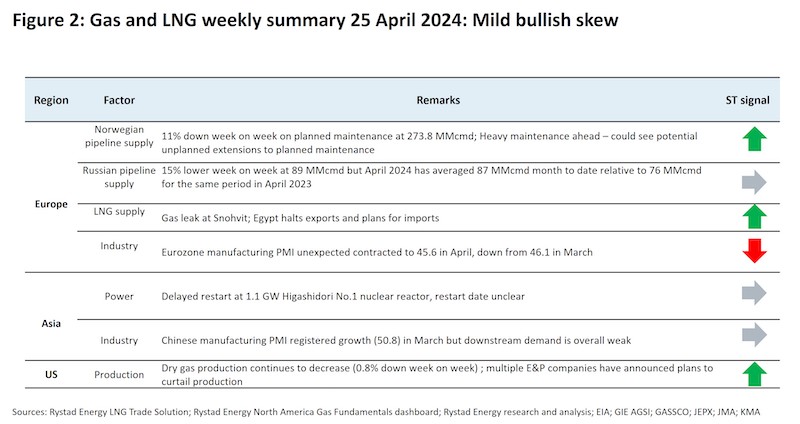

Meanwhile, amidst maintenance and a recent gas leak at Snohvit LNG, Norwegian pipeline issues altered Europe's LNG exports, decreasing supply by 11% week-on-week to 273.8 million cubic meters per day (MMcmd)."

Global gas markets have had an eventful April, with the Title Transfer Facility (TTF) and Asian spot prices briefly rising to $10.44 per million British thermal units (MMBtu) and $10.46 per MMBtu, respectively, in the third week of the month after missile attacks between Iran and Israel.

However, the prospect of a runaway escalation appears to have receded (but has not disappeared), as have the TTF and Asian spot prices, to $9.2 per MMBtu and $10.135 per MMBtu, respectively.

Despite some bullish signals towards the northern summer, the upside risk remains capped due to weak demand in price-making regions.

Europe

Norwegian pipeline supply is down 11% week-on-week to 273.8 million cubic meters per day (MMcmd).

Heavy maintenance is scheduled in the weeks ahead that could support prices, with May supply expected to average 296 MMcmd, although this is higher than the 262 MMcmd of May 2023.

Norway’s Snohvit LNG reported a gas leak on 23 April during planned maintenance.

The market has not noticed this much, as the facility is expected to restart on Friday.

Snohvit provided 5.8% of Europe’s LNG imports in March.

Egypt has turned to LNG imports driven by lower-than-expected output from the Zohr gas field (which recently had a reserves downgrade) and rising domestic demand.

Egypt has already imported an LNG cargo this year through Jordan and is understood to have chartered an FSRU for direct imports at Ain Sukhna from June onwards.

The country provided around 2% of Europe’s LNG imports in May 2023 but is not expected to export at all in May 2024.

Russian pipeline gas volumes have averaged 87 MMcmd in April month to date, up from 76 MMcmd for the same period last year.

Their impact has largely faded from public memory, but the market will be watching for the effect of the expiry of the transit deal with Ukraine.

On the bearish side, the Eurozone manufacturing purchasing managers index (PMI) contracted unexpectedly in April to 45.6, down from 46.1 in March, underscoring the weak macro-outlook for the industrial sector.

March 2024, gas consumption in the EU27 and the UK was 4.5% lower year-on-year, driven by reduced gas for power and residential consumption.

Asia

In Japan, the delay in restarting Tohoku Electric’s 1.1 gigawatts (GW) Higashidori nuclear reactor could drive demand for replacement fuels.

The reinforcement work at the reactor was previously expected to be completed in the current financial year (April 2024- March 2025), but the completion date is now unknown.

Chinese manufacturing PMI data registered growth in March (50.8) for the first time since September 2023.

However, overall downstream gas demand remains weak, and we will wait to see if the momentum sustains before marking this as a bullish indicator for prices.

US

The Henry Hub has been unchanged week-on-week at around $1.7 per MMBtu, driven by oil-directed production growth from the Permian and weak demand from ongoing mild temperatures.

For the week ending 12 April, gas volumes in storage stood at 2,333 billion cubic feet (Bcf), 22% higher year on year.

With the US now producing 7.7% of Asia’s LNG imports, low Henry Hub prices at levels of $1.7 per MMBtu imply a potential price floor for Asian spot prices at around $7 per MMBtu, which reflects the total cost of a US-loaded cargo delivered to East Asia.

There is likely limited room for the Henry Hub to decline further, given widespread gas production curtailments from multiple exploration and production (E&P) companies.

EQT most recently extended a production curtailment of 1 billion cubic feet per day (Bcfd) through May.

Follow us on social media: