The Freeport LNG blast spells trouble for Europe but opens a potentially lucrative opportunity for North and West African gas exporters to fill the gap. Lockdown lifts in China should see demand rise, but buyers are in no rush to purchase as they can still access Russian LNG. Highlighting the different approaches that governments can take depending on their relations with Russia, neighboring Japan imported more LNG in May than China.

Here is Rystad Energy’s regular gas and LNG note from analyst Zongqiang Luo

The Freeport LNG blast spells trouble for Europe but opens a potentially lucrative opportunity for North and West African gas exporters to fill the gap. Lockdown lifts in China should see demand rise, but buyers are in no rush to purchase as they can still access Russian LNG. Highlighting the different approaches that governments can take depending on their relations with Russia, neighboring Japan imported more LNG in May than China.

On 8 June, the Freeport LNG facility reported an explosion and fire.

While no injuries were reported, the Freeport facility has announced the plant will remain shut for three weeks however the possible extend of the damage to the facility is yet to be determined and it may be out of service for longer.

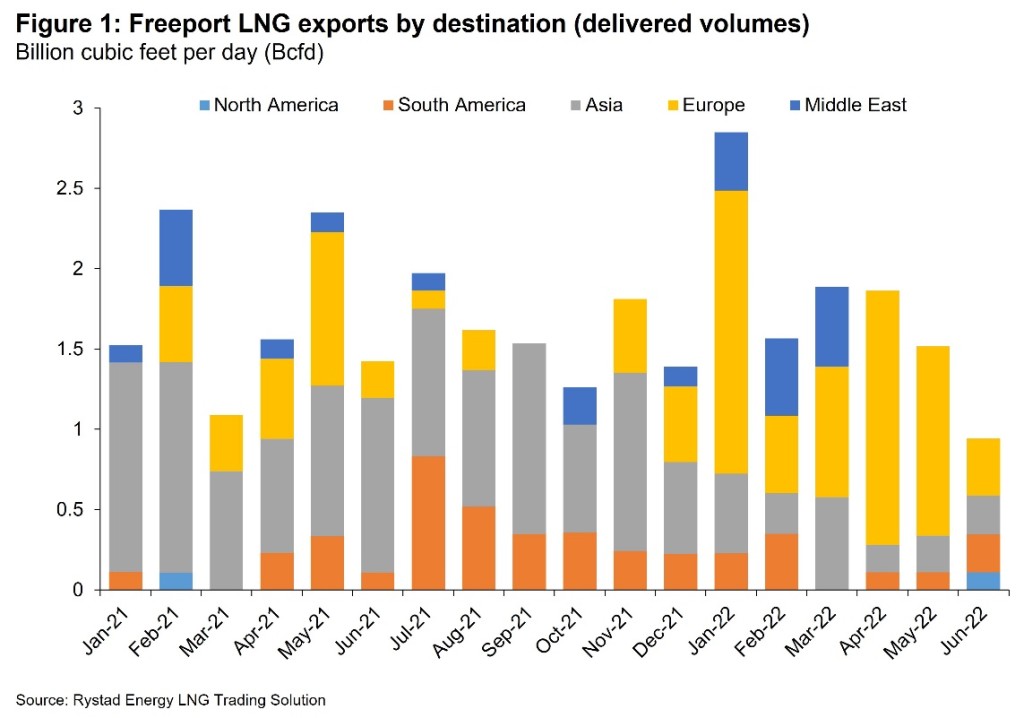

The Freeport LNG facility has a capacity of around 2 Bcfd and had been running close to capacity in recent months.

Since Russia’s invasion of Ukraine at the end of February 2022, the bulk of volumes have ended up in Europe, rising from about 0.81 Bcfd in March to 1.17 Bcfd in May 2022.

Freeport LNG has been flexible and quick to divert volumes to Europe since on average around 76% of its exported volumes in 2022 are uncontracted, as a result, we expect Europe will be the region most impacted by this incident.

Freeport LNG exports to Europe account for about 10% of total import volumes into Europe.

The region relies heavily on US export volumes which have accounted for approximately 45% of imports since the start of the year.

Russia and Qatar each account for about 15% of Europe’s import volumes with the remaining third coming from Nigeria, Algeria, Southern America and the Caribbean.

Since the Russian invasion, uncontracted volumes from Freeport have found their way to European markets, reducing its exposure to the Asian market.

More recently, Freeport to Europe has been a popular route for vessels such as Corcovado LNG, Yiannis, Maran Gas Andros, Prism Courage and Prism Brilliance that are chartered by JERA, Osaka Gas and SK E&S and are typically used to supply volumes to the Asian market.

While Freeport LNG is offline, it is unclear which alternative volumes could replace the drop in exports to Europe.

However, with favorable spot prices, countries such as Nigeria and Algeria that are producing well below capacity could increase production to help fill the void.

Additionally, US uncontracted spot volumes from larger exporting facilities including Sabine Pass, Corpus Christi, and Cameron LNG could divert supply to Europe.

Currently, Henry hub natural gas futures was closed at $8.85 per MMBtu on 10 June after hitting the 14-year high of $9.7 per MMBtu earlier last week with news of the explosion at Freeport LNG facility and uncertainty around the near-term gas demand though a blistering summer is expected.

Europe

Though the TTF gas price gained $1.5 per MMBtu to settle at $26 per MMBtu on 8 June with the news of Freeport LNG explosion and continuous drop of the Russian pipeline gas volume, it settled at $25.51 per MMBtu primarily driven by Europe’s gas inventory build-up and strong injection.

A total underground gas injection volume of 35.12 billion cubic meters (Bcm) has been seen in the first 5 months of 2022 with the depleted storage level after the 2021 winter and the gas injection in June is averaged at 477 million cubic meters (mcm) per day, which is 17% (or 76 mcm per day) higher compared to previous year.

Therefore, the current European underground storage level has reached at 57.11 Bcm on 11 June and the strong injection is estimated to continue during the summer as the European Commission’s storage target was set to meet 80% minimum gas (or approximately 84 Bcm gas) by 1 November 2022.

In terms of piped gas, Russian gas supplies to Europe via the main three routes continue to decline to 170 mcm per day which is close to the level at the beginning of 2022.

The main cause of the flow decline is less supplies via Ukraine transited volume as one key transited gas delivery point at Sudzha did not receive re-directed gas from Russia since the full stop of gas supplies via Sokhranivka pipeline in early May.

Meanwhile, the annual maintenance of Nord Stream 1 is scheduled to happen between 11 July 2022 and 21 July 2022 according to Nord Stream AG.

So far, the Nord Stream 1 gas supplies are the most stable route for Europe and the coming 10-day maintenance work would mean a gas supplies loss of 1.55 Bcm for Europe during the summer, which would further tighten the European gas market.

Asia

In China with the full lifting of covid lockdown in Shanghai Chinese gas consumption in the commercial sector and industrial sector are estimated to partially recover in June.

However, Chinese buyers are not in a hurry to secure more LNG cargoes as they have relatively sufficient LNG inventories for the summer months.

In May, Japan had imported about 5.43 million tonnes of LNG surpassing the Chinese LNG purchases of 4.93 million tonnes.

Japanese LNG imports will probably continue to grow as the closure of units of the coal-fired and the biomass-fired power plants of JERA to meet the gas-for-power demand during the summer peak months.

Therefore, we except that the JKM price will fluctuate in the range between $23 per MMBtu and $26 MMBtu in the following months.

Follow us on social media: