The European Commission published the final draft of its Critical Raw Materials Act (CRMA), which identifies a list of strategic raw materials and sets clear benchmarks for domestic capacities along the strategic raw material supply chain with the aim of diversifying the EU’s supply chain by 2030.

Among strategic battery raw materials, graphite is likely to be the biggest headache for the EU as it seeks to lessen its dependence on China.

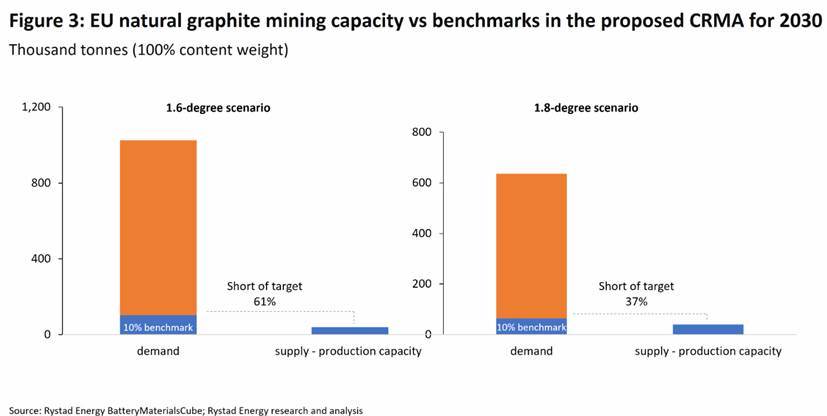

In the upstream mining, the Act specifies that domestic extraction capacity should be able to extract the ores, minerals or concentrates needed to produce at least 10% of the EU’s annual consumption of strategic raw materials to the extent that the EU’s reserves allow this.

In the processing sector, the proposed Act states the domestic processing capacity, including for all intermediate processing steps, should be able to produce at least 40% of the EU’s annual consumption of strategic raw materials.

Graphite is the biggest bottleneck as the EU only has limited mining capacities where natural graphite is concerned and limited processing capacities for spherical graphite – the processed material of natural graphite and key material to produce anode active materials after further purification or coating.

In the optimistic demand scenario, the EU will consume 1.03 million tonnes of graphite in 2030, with 10% of consumption sitting at 102,630 tonnes. Meanwhile, the natural graphite mine production in the EU is estimated to be 39,900 tonnes in 2030.

In other words, the domestic natural graphite mining capacity is 61% short of the target.

In the base case demand scenario, the natural graphite mining capacity in the EU is 37% short of the target.

China will continue to dominate natural graphite mining for the foreseeable future, although Canada and some African countries, including Mozambique, Tanzania, and Madagascar, are going to contribute increasingly more to the natural graphite supply in the next few years.

Compared to its mining capacity, graphite processing is even more of a challenge for the EU given the limited number of spherical graphite projects in the region, and a majority of which are still at a very early stage of development.

In other words, to meet the benchmark requirement of 40% consumption of natural graphite, the EU needs to work hard to build up its own processing capacities.

Apart from natural graphite, the EU also needs to raise its processing capacities on manganese as battery demand increases.

In the optimistic demand scenario, the EU sees its domestic processing capacities 26% short of the required percentage of consumption in 2030.

The EU might be able to achieve the benchmark set for lithium, cobalt and nickel in 2030 given announced processing capacities in each market.

That said, processing capacities are not equal to actual production, therefore, whether the actual production of relevant processed materials of lithium, cobalt and nickel can meet the benchmarks stated in the Act is still subject to the operational rates in 2030 and whether relevant processing plants can be put into operation as scheduled.

The Act also flags many strategies to ensure the EU’s access to a secure, diversified, affordable and sustainable supply of critical raw material, including setting up a maximum lead time for permitting strategic projects.

However, it hasn’t touched upon any point of specific incentives for stakeholders along the battery supply chain in the proposed Act.

When comparing the EU Critical Raw Materials Act with the US’ Inflation Reduction Act, so far, it seems the US has more incentivizing points for industry.

The EU shifts focus on charging infrastructure in ambitious new law

On Tuesday, a provisional agreement was reach in the European Council indicating a large overhaul on infrastructure rules for alternative fuel powered vehicles in the EU, specifically across the Trans-European Transport Network (TEN-T).

Among many things, this network is intended to connect various sections of transport in the EU, alleviating long-distance traffic and linking peripheral regions to centra regions of the EU.

The new proposal aims to improve public charging infrastructure and provide ease of accessibility and usage to end consumers.

- For Cars (M1) and Vans (N1): given rapid uptake in both segments, charging infrastructure deployment will grow at the same pace as vehicle uptake. For every BEV in the fleet of a country, a minimum power output of 1.3 kW must be provided in public charging points. Across the TEN-T network, starting 2025, fast charging stations with power level above 150 kW will be installed every 60 kilometers, and full coverage must be achieved by 2030.

- For Heavy Duty Vehicles (M2, M3, N2, N3): Special focus is placed on improving the fast-charging network. Starting 2025, DC charging stations must be installed with power output of minimum 350 kW every 60 kms on the core TEN-T network, and every 100 kms on the comprehensive network, with full coverage by 2030. Power output should reach 1.4 MW to 2.8 MW depending on the traffic density of the road. These will also have to be supported by installation in secure areas for overnight charging, and special focus must be placed in urban nodes for intra city delivery vehicles.

With special emphasis being placed on charging station installations on sections of the road defined by kilometers will lead to more densely populated areas having more charging stations installed. For example, Germany has 11,000 kilometers of road on the network with 6000 kms of road on the core network.

Under the new laws, by 2030, Germany would have to install 100 fast charging stations for M1 and N1 vehicles, and 1100 DC points above 350 kW for heavy-duty vehicles, of which 600 must be on the core network.

As such, most countries in the EU have their own charging station installation requirement but mandating installations across highways will especially benefit heavy-duty vehicles. Battery Electric Trucks with payload above 14 tons have higher TCO than their diesel counterparts mainly due to time lost in charging.

Implementation of charging stations delivering power above 1 MW (dubbed the Megawatt Charging System) will significantly reduce this time and lead to faster adoption of battery electric trucks and buses.

Follow us on social media: