The European Union’s emergency measures to tackle the region’s energy crisis may fall short of their intended goals, at least where renewable energy ambitions are concerned, according to Rystad Energy research. The EU’s proposal to temporarily cap the revenues of inframarginal electricity producers is aimed at capturing the windfall profits of renewable energy producers, which are benefitting from low production costs during this episode of high electricity prices.

However, research by Rystad Energy reveals that about 60% of the total installed renewable energy capacity in the EU derives its revenues from fixed-rate contracts agreed well before the energy crisis – with prices generally below current spot prices. According to the EU Commission, an estimated €117 billion would likely be collected by implementing a revenue cap on low carbon and coal power generation, but the windfall profits described by the EU account for only 40% of renewable energy producers. Indeed, the revenue distribution of installed capacity in Europe shows that less than half of the generation capacity would fall under the aims of the revenue cap policy.

Claims that renewables are making windfall profits during the crisis are therefore more complex than the European Commission and others suggest. Targeting all types of plants with such a non-tailored policy confuses the market and calls into question the effectiveness of the response. At a time when the EU should be accelerating the pace of renewable energy deployment, it instead runs the risk of sending a warning signal to investors, while leaving the pressing issue of future capacity installment unaddressed.

Rystad Energy therefore expects investors and developers may be scared off, which could lead to lower investments, delays to projects, and the renegotiation of long-term contracts for projects still under development. Given the Commission’s ambitious new targets for renewables, it would seem sensible to also tackle the actual issues facing the sector: permitting, auction prices and supply chain support – as the USA did with the recent Inflation Reduction Act.

“The EU’s unprecedented intervention, while necessary, is temporary and does nothing for the medium to long term supply gap issue. The renewable industry is Europe’s best shot at producing affordable and secure power, but this policy reduces the private sector power providers ability to invest. The renewable power industry is not only helping to keep the lights on in Europe, but also picking up the bill too. If renewables are to take their proper place in Europe’s power mix, they will need support in turn in the not-too-distant future.

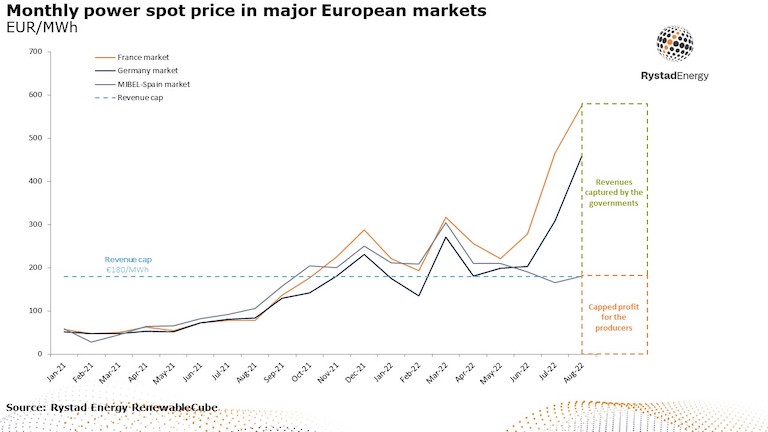

In recent months, power prices have reached record-high levels, averaging over €500/MWh in August, and record daily and weekly prices exceeding €700/MWh. Consequently, the EU and its member countries are aiming to implement a cap on renewables profits – proposed at €180/MWh regardless of the market timeframe in which the company sells the electricity. This cap would apply to wind, solar, biomass, nuclear, lignite and some hydroelectric plants. Revenues above the price cap will be redirected to member states and used to help households and businesses facing financial stress due to soaring energy bills. According to the Commission, an estimated €117 billion would likely be collected by implementing this measure.

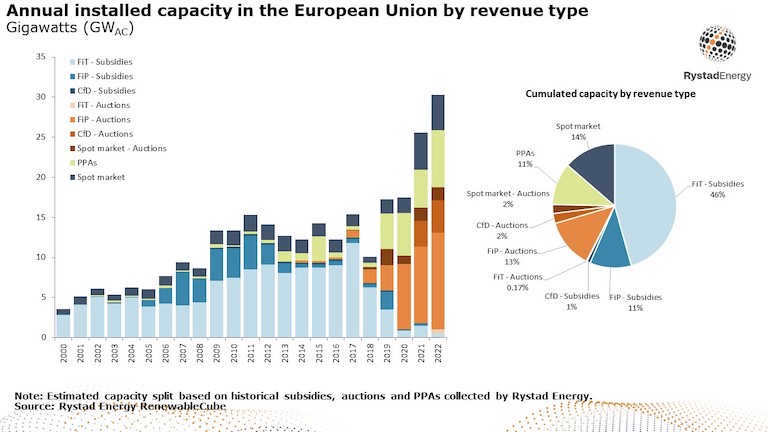

While the revenue cap would apply to all renewable energy plants, only about 40% are benefiting from the current crisis. Since 2000, most European governments have put in place subsidy policies to incentivize renewable energy development. These schemes, known as feed-in-tariff (FiT), feed-in-premium (FiP), and contract-for-differences (CfD), have been widely subscribed to by early renewable energy developers, as they offered lucrative offtake tariffs relative to average electricity prices. These historical subsidies, lasting between 15 and 25 years, now account for more than half of the region’s installed capacity, with support distributed across the different schemes. The prices of these bilateral agreements are on average lower than current electricity prices. Since 2015, governments considered these subsidies too lucrative for renewable producers and gradually replaced them with auctions. Most auctions in Europe award capacities with schemes like FiT, FiP, and CfD but allow governments to offer these competitive tariffs based on a bidding process. Other auction schemes provide fixed subsidies and producers must sell the produced power on the spot market.

Rystad Energy estimates that 17% of the total capacity installed today is subsidized through auction schemes, notably in Germany, Spain, and France. In addition, power purchase agreement (PPAs) gained popularity after 2010, and were either concluded with companies, utilities, or governments. PPAs allow for fixed tariffs negotiated according to market conditions at the time and represent 11% of total renewable energy capacity installed today in the EU. Finally, the remaining capacity (14%) receives revenues directly from the spot market. These may be plants that started up in the early 2000s and for which the subsidy contract has since expired or have opted for the spot market combined with a hedging strategy or, more recently, that have bet on a sufficiently-high power price to reach profitability.

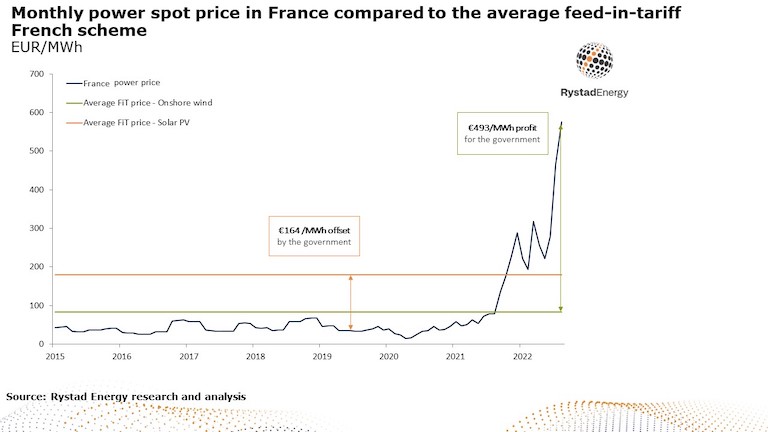

Among these different mechanisms, two types of revenue streams are key to understanding the current situation: fixed revenues and market-based revenues. Fixed revenues come from fixed tariff contracts like the FiT, CfD or PPA contracts (awarded through subsidy schemes or auctions). In total, these contracts represent 60% of the total installed renewables capacity in the EU (170 GW), mainly distributed between Germany, France, and Spain. Producers operating this capacity cannot make windfall profits on high electricity prices, as they are obliged to redistribute revenues above the negotiated price to the counterparty in the agreement. On the other hand, current market conditions have led to a significant shift – after 20 years of governments having to pay a fixed above-market price to renewable energy developers, governments are now making a profit. In France, the government offered FiT subsidies for onshore wind between 2000 to 2015, with an average tariff of €82.6/MWh and a duration of 15 years. Based on last month's average electricity price, the French government made an average profit of €493/MWh. More recently, the French Energy Regulatory Commission (CRE) announced that renewable energy revenues for 2022 and 2023 are expected to total €8.6 billion for the state budget. This is the first time that these revenues are positive, which directly reflects the current trend.

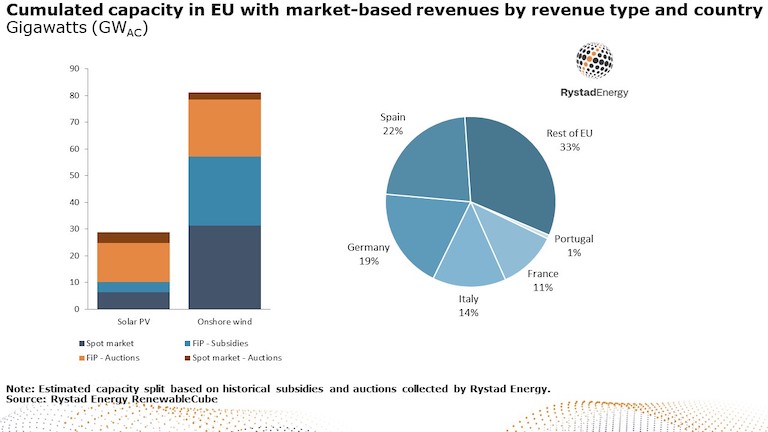

The opposite side of the story concerns market-based revenues, i.e., capacity with a spot price risk. This includes revenues derived from FiP schemes, contracted through auctions or subsidies. The difference with the FiT contract lies in the way revenues are calculated. The level of payment is based on a premium offered as government subsidy above the electricity market price. This premium can be constant or vary according to a sliding scale. While this mechanism was used to avoid the risk of overcompensation, ironically, it is now the main source of windfall profits for producers. Indeed, producers with FiP contracts now benefit from high power prices and a constant premium, depending on the schemes. As renewable energy revenues vary between a fixed rate and a market-based rate, the relevance of such a policy is questionable.

As the implementation of policies to manage the market is inherently complex, the Commission decision to propose a constant cap regardless of the types of revenues and market specificities has led to great confusion over its impacts. At a time when renewables are being urged to address the dual energy and climate crisis, this policy sends out a negative signal to the sector. Once intervention of this size and scale begins in a market as essential as energy the impacts are myriad and likely to require further intervention.

Follow us on social media: