Since the start of COVID-19, the nature of air cargo developments has changed dramatically. All sorts of changes, unheard of up till 2020, could be seen in the past four months. We have reported on the market meltdown. We have noted the dramatic drops in capacity. We have shown the enormous impact on air cargo cost of the sudden need for goods, essential for combating the virus. We have seen weekly changes hitherto unknown (in capacity, in load factors, in ‘new’ aircraft types, in airline yields, etc.). Today, we can provide the picture on the first half of the year, thanks to the fact that almost all airlines in WorldACD have reported to us their full figures through June.

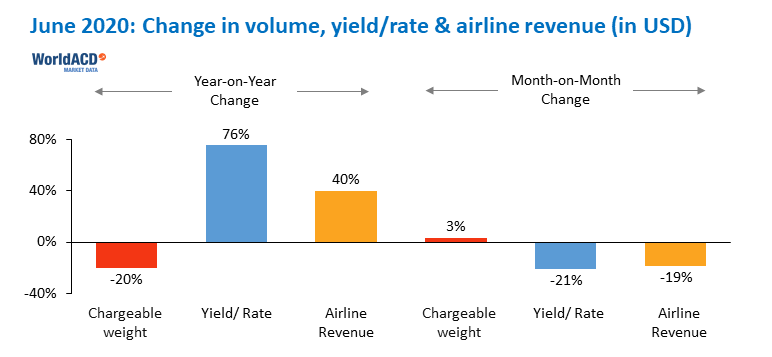

Most airline bosses had great worries in H1-2020, but a lack of cargo revenue was not among them… Though worldwide volume YoY (year-on-year) contracted by more than 18% in H1-2020, revenue in USD increased by almost 21%, thanks to the capacity shortage as from Mid-March. In terms of volume, the origins Middle East & South Asia (MESA) and Europe suffered most: -32% resp. -22%. In incoming traffic, Asia Pacific and Europe each lost 16% YoY, while other regions lost more. The average rate of transporting one kilogram by air rose by 48% worldwide: the increase was largest from Asia Pacific (+76%) and smallest from Latin America (+10%).

The YoY volume decline in H-1 was smallest in business originating in the Asia Pacific region. Volumes from this region to Europe and North America were hit much less (-6% resp. -11%) than volumes to e.g. MESA (-15%). Thanks to the demand for Personal Protection Equipment (PPE), China did not show any decrease in volume YoY and remained flat, but the transport of these PPE-goods did not come cheap: air cargo charges from China rose by an incredible 136% compared to the first half of 2019. As large parts of the world were in turmoil, demand for flowers fell less than average (-16%). The volume of high tech & other vulnerable goods dropped by 6% only, whilst the transport of pharmaceuticals, the evergreen in air cargo, grew with +8% YoY.

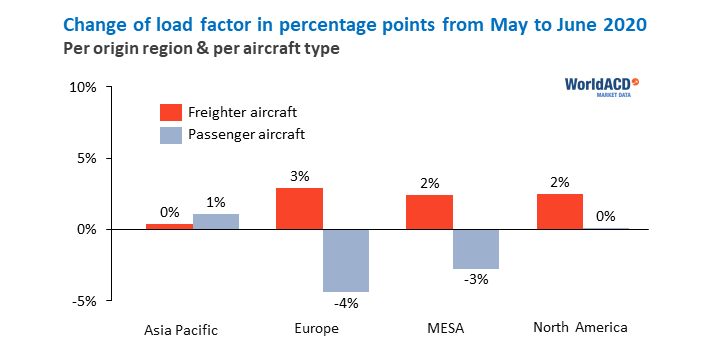

Looking at month-on-month (MoM) developments from May to June, we saw worldwide volumes increase with almost 3.5%. Coupled with a decrease in USD-yields of 21%, this resulted in a MoM revenue decrease for airlines of 19% measured in USD. In other words, the extreme results of April and May (great volume loss coupled with a large revenue increase) diminished somewhat. However, the sector is still far from what it used to be, as June worldwide showed a YoY volume decrease of 20% and a yield increase of 76%...

The first weeks of July do not seem to change the present picture very much: yields have not returned to “pre-COVID-levels”. Based on the largest set of market data inputs available in air cargo, we make the very provisional statement that worldwide yields dropped by no more than 2.4% from the last week of June through the first two weeks of July (from Asia Pacific and MESA by 4% resp. 3%). And weekly volumes were lower by mid-July than two weeks before.

But a word of caution is called for when looking at data from the most recent weeks. Understandably - given the high market volatility - we have recently seen a flurry of weekly air cargo figures being reported. At WorldACD, we have learned over many years that part of the data on air cargo transactions are subject to some degree of correction when data for the full month are assembled and finalized. Data may also be based on too small a sample to be truly representative, or may be just anecdotal evidence.

As WorldACD’s commercial director Ken de Witt Hamer puts it: “Every data provider, WorldACD included, should be careful with weekly data. They are potentially interesting indications of market movements, but they can only be more than that if based on a robust set of final transactional data. Of course, it is up to data consumers to assess their value, to separate the wheat from the chaff, so to speak.”

Follow us on social media: