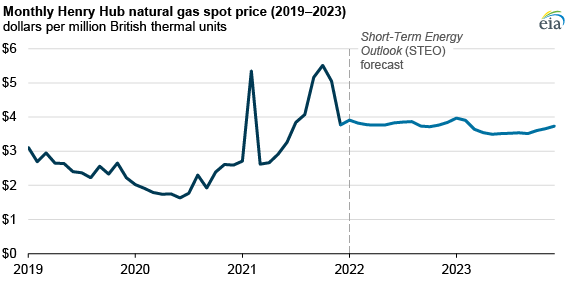

In our January Short-Term Energy Outlook (STEO), we forecast that the natural gas spot price at the U.S. benchmark Henry Hub will average $3.79 per million British thermal units (MMBtu) in 2022, slightly less than its 2021 average of $3.91/MMBtu. Natural gas prices increased between March and early October 2021, but they declined in the last three months of the year. We expect natural gas prices to decline slightly in 2023, averaging $3.63/MMBtu, as growth in dry natural gas production outpaces growth in domestic demand and exports.

Recent volatility in the natural gas spot price at the Henry Hub near the end of 2021 contributed to increased uncertainty in our price forecast. Deviations from winter weather expectations, the potential for extreme weather events such as this past year’s February cold snap, and a rise in demand for natural gas imports in Europe and Asia—where spot prices have reached record highs in the past few months—all have contributed to the recent variability in natural gas prices.

We forecast that the Henry Hub spot price will remain relatively flat for most of 2022. Forecast growth in U.S. natural gas production and relatively unchanged domestic consumption leads to continued growth in U.S. natural gas exports. We expect natural gas prices to begin to decline in 2023 as production grows, U.S. liquefied natural gas (LNG) exports and pipeline exports to Mexico increase slightly, and consumption in the industrial and electric power sectors remains similar to 2022 levels.

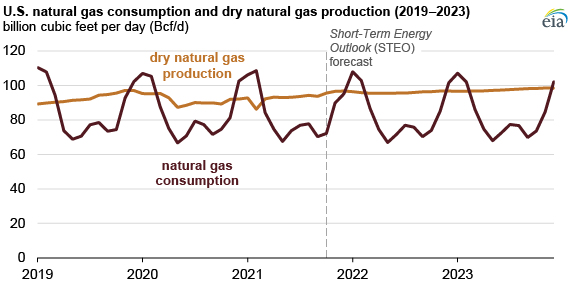

We expect domestic dry natural gas production to grow 2.7% to a record-high 96.0 Bcf/d in 2022 and to 97.6 Bcf/d in 2023. We forecast annual U.S. natural gas consumption will remain relatively unchanged in 2022 and increase slightly in 2023. Consumption increases in 2023 because natural gas is increasingly used in the industrial sector and is only slightly offset by a decline in natural gas consumed in the electric power sector as more renewable electric power plants are installed.

We expect U.S. exports of natural gas—both by pipeline to Mexico and Canada and in the form of LNG to overseas destinations—to continue to grow, especially as new U.S. LNG terminals come online and reach full utilization.

Principal contributor: Max Ober

Follow us on social media: