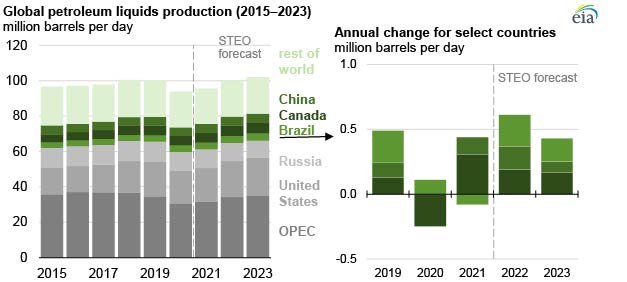

In our June 2022 Short-Term Energy Outlook (STEO), we forecast that liquid fuels production in Brazil, Canada, and China will increase this year and next, contributing to growth in overall non-OPEC petroleum production. We forecast that petroleum production in the combined non-OPEC countries, excluding the Unites States and Russia, will increase by 3% (0.9 million barrels per day [b/d]) in 2022 and by 2% (0.8 million b/d) in 2023, compared with an increase of less than 1% (0.2 million b/d) in 2021.

The United States will account for about 60% of the growth in combined liquid fuels production in all non-OPEC countries. After the United States, we expect liquid fuels production to increase the most in the non-OPEC countries of Brazil and Canada. By the end of 2023, Brazil's liquid fuels production will increase by 400,000 b/d, and Canada's will increase by nearly 400,000 b/d to 5.9 million b/d.

For Brazil, our forecast assumes that production from six new floating production storage and offloading (FPSO) units will ramp up through 2023 and continue to drive growth, notably at the Sepia, Mero, and Buzios fields. Once they reach full capacity, these FPSOs will each produce between 70,000 b/d and 180,000 b/d of liquid fuels. We expect Brazil’s production to increase from 3.7 million b/d in 2021 to 3.9 million b/d in 2022 and to 4.1 million b/d in 2023.

Canada’s growth in crude oil and natural gas production during 2022 and 2023 is driven primarily by expanding oil sands and debottlenecking projects. Canada’s growth is due in part to the Enbridge Line 3 crude oil pipeline expansion (760,000 b/d capacity), which became operational in October 2021. The TransMountain pipeline expansion project (890,000 b/d capacity) is slated to enter service at the end of 2022. Additional Enbridge expansions and optimizations to its existing pipeline system, if completed, will add more than 400,000 b/d of export capacity through 2023. Due to this new pipeline capacity from Enbridge and other planned pipeline expansions, current constraints on oil exports from Canada are expected to lessen by the end of 2023 and drive increased production.

We forecast that liquid fuels production in China, which increased by 130,000 b/d in 2021, will grow by an additional 170,000 b/d in 2022 and 80,000 b/d in 2023 in response to government calls for increased exploration and production. The remaining key sources of forecast non-OPEC production growth come from Norway, Argentina, Kazakhstan, Oman, and Guyana.

Follow us on social media: