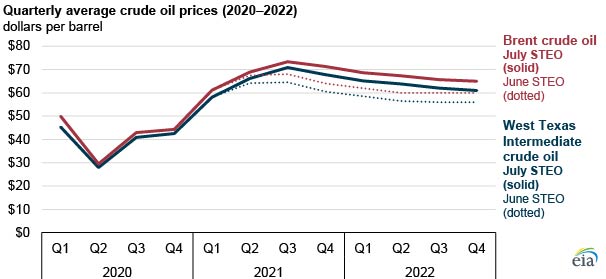

In the July Short-Term Energy Outlook (STEO), we forecast the Brent crude oil price will average $72 per barrel (b) in the second half of 2021 (2H21) and $67/b in 2022, both $6/b higher than in the June STEO forecast. We revised global production down by 210,000 barrels per day (b/d) in 2H21, leading to larger forecast inventory draws in 2H21 and smaller forecast inventory builds in 2022, which contributes to the increased price forecast.

In the July STEO, we forecast the Brent crude oil price will average $73/b in the third quarter of 2021 (3Q21) and will fall to average $71/b in the fourth quarter of 2021 (4Q21). Also in the July STEO, we forecast the Brent crude oil price will fall from an average of $69/b in 2021 (up from $65/b in the June forecast) to $67/b in 2022 (up from $60/b in the June forecast). We also expect West Texas Intermediate (WTI) crude oil prices will likely follow a similar path. WTI crude prices are forecast in the July STEO to average $71/b in 3Q21, $6/b higher than in the June STEO. The July STEO expects WTI prices to be $68/b in 4Q21, up $7/b from the June forecast.

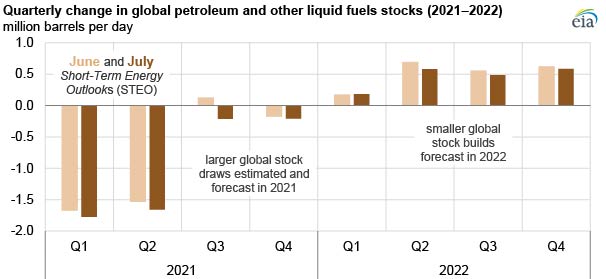

The Brent crude oil price averaged $73/b in June 2021, up $5/b from May. June was the first month when the Brent price averaged more than $70/b since May 2019. We expect moderate downward oil price pressures will emerge beginning in 2H21, when forecast global oil production will rise, causing inventories to draw at a slower pace. Significantly smaller stock draws in 2H21 compared with 1H21 and stock builds in 2022 will likely put downward pressure on oil prices. In the July STEO, we forecast implied global stock draws (the difference between consumption and production) of 210,000 b/d in 2H21, a significant increase from average stock draws of 20,000 b/d in last month’s forecast but still significantly less than the average draws of 1.7 million b/d in 1H21. We expect implied stock builds in 2022 will average 460,000 b/d, down from 510,000 b/d in last month’s forecast.

From June to July, we lowered the global petroleum production forecast by nearly 210,000 b/d in 2H21, driving the larger stock draws in the forecast. We also lowered our forecast of OPEC production of crude oil, the largest driver of the downward revision, by 110,000 b/d in 2H21. For 2022, we made minor, offsetting revisions to U.S. and OPEC production forecasts, resulting in the global petroleum production forecast remaining at 101.8 million b/d in the July STEO.

Follow us on social media: