But with global economies slowing, where will it end up?

China’s zero-COVID measures placed severe restrictions on the country’s economic activities. But late in 2022, faced with growing public demands to end the lockdowns, the government did an about face and reopened the economy.

That risky reversal led to increased levels of COVID infections and deaths, in the short run, and additional localized lockdowns, but the spread of the virus was reported to have abated relatively quickly. Another result of the policy change was a jump in steel production in China, thanks to the reopening of factories. It still remains to be seen, however, whether those increased volumes of steel will be able to be absorbed domestically and or internationally.

Steel: Mixed Results

Many economists are insisting that a global economic downturn is in store, which would depress steel demand, although the data have been mixed. Reading the tea leaves when it comes to China’s economy and its steel industry, on the other hand, yields a decidedly negative outlook.

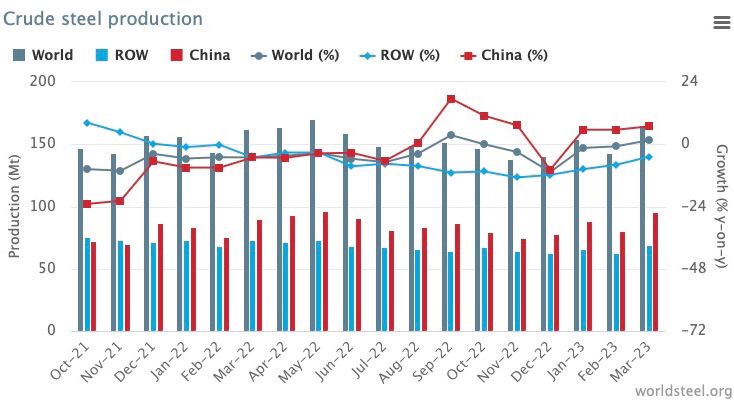

The World Steel Organization (WSO) reported that China’s steel production in March was up 6.9% compared to March 2022 and 6.1% year to date. Those figures grew on February’s numbers, which showed a 5.6% increase over February 2022, and the same year to date. Global production increased by 1.7% in March and decreased by 1.0% in February.

China’s March performance outpaced other major steel producers by a long shot. India’s steel production was up 2.7%, as was Italy’s, while Russia’s and Germany’s output remained flat. Japan, the United States, Brazil, and Turkey were all down, the latter two by 8.7% and 18.6%, respectively.

Steel rebar futures traded in Shanghai have been plummeting of late, by over 15% as of late April, from a recent high in mid-March. The late-April figure of $528 per ton was the lowest in over five months, according to Trading Economics, reflecting “deepened concerns over weak demand in China.

“The recovery of construction and infrastructure activity in China failed to materialize,” Trading Economic commented, “despite the country’s reopening and a round of government stimulus and liquidity injections.”

New construction starts in China dropped by over 20% during the first quarter of 2023, government data show, and property investments decreased by 5.8%. An April survey showed iron ore inventories in Chinese ports up 1% over a week, “pointing to limited demand from steel producers,” Trade Economics said. A Chinese steel industry group is urging producers to cut output, and reports indicate that the government could reduce production by 2.5% this year.

China Steel Demand

According to Worldsteel, China’s total steel demand declined by 3.5% in 2022, is expected to grow by 2.0% in 2023, and to stay flat in 2024. By contrast, global demand will see a 2.3% rebound this year and 1.7% growth in 2024.

“In 2024, demand growth will be driven by regions outside China but faces global deceleration due to China’s anticipated 0% growth, overshadowing the improved environment,” said Máximo Vedoya, CEO of the Luxembourg-based steel manufacturer Ternium, and chair of the Worldsteel economics committee. “As China’s population declines and moves to consumption-driven growth, its contribution to global steel demand growth will lessen.”

The property sector in China is a major consumer of steel, but “all key real estate indicators are in deeply negative territory,” noted a recent Worldsteel report. Floor space of newly started projects and total real estate investments are showing steep declines, “the first year-on-year decline in 25 years.” The organization expects “a slight pickup” in the real estate sector this year “due to government support measures,” with a “moderate” recovery expected to continue in 2024.

At the macroeconomic level, the Chinese economy saw 3% growth in 2022, well short of the government’s 5.5% goal. And, according to a report in Foreign Affairs, “the real rate may have been worse,” as “official statistics are increasingly dubious.”

Long-Term Prospects

Long-term prospects for economic growth under any scenario, according to the report, will not match China’s growth rates since it embraced economic reforms in the late 1970s. As a United Nations population report noted, China’s population is aging, and its working-age population is shrinking.

In addition, “a rash of business and bank defaults, fiscal shortfalls for heavily indebted local governments, and falling returns on investment,” according to the Foreign Affairs report, all point to slower growth in capital investments.

Besides all that, Chinese government policy is now moving in the wrong direction. “Chinese officials sanctioned more state control and more administrative intervention in the allocation of capital,” the Foreign Affairs report stated. “If leaders remain fixed on statism, the growth rate might rise somewhat for a year or two, but then it will fall to potentially 2% or lower in the second half of this decade. If China re-embraces reform, growth would drop even lower through the medium term but could then climb back to potentially 4% as 2030 approaches.”

In either case, the report concluded, China’s “days of super-high growth are over.”

If there is a silver lining for China’s steel industry, it is that global steel demand is expected to grow this year and next. Worldsteel expects steel demand in developed economies to increase by 1.3% in 2023 and 3.2% in 2024. Demand growth in the U.S., at 1.3% in 2023, will match global growth, but the expected growth rate of 2.5% in 2024, will fall short. The 2021 infrastructure law, the Inflation Reduction Act, and “expanding energy production” are all expected to contribute to demand growth in the U.S., according to Worldsteel.

China’s neighbors in Asia represent better potential export markets. The Indian economy, according to Worldsteel, will see “healthy growth” thanks to government infrastructure spending, stronger residential housing demand, investments in renewable energy, and spending on automobiles and consumer durables. Worldsteel expects demand in India to grow by 7.3% in 2023 and 6.2% in 2024. The ASEAN nations also represent bright spots, where steel demand is expected to increase by 6.2% in 2023 and 5.7% in 2024, fueled by major projects such as building Indonesia’s new capital in East Borneo, development of long-distance railways in the Philippines, and infrastructure spending in Vietnam.

Follow us on social media: